The Banking sector is susceptible to operational risk due to its complexity, its dependence on technology, and the variety of activities it undertakes. As part of Indonesian bank, Bank ABC already has the risk management governance and is actively supervised by board of commissioners and board of directors. Nevertheless, a significant amount of operational loss is still recorded every year. It was found that the main contributor was the case of excess payments of pension benefits to the heirs of customers who had passed away. This research combines both qualitative and quantitative methods. The primary data were collected from in depth interviews with subject matter experts (SME), analysis using Business Process Modeling Notation, Business Blueprint, and identifying the critical root cause using Theory of Constraint. While the secondary data from internal system Bank ABC. The undesirable effects will be addressed using the selected solution from Analytical Hierarchy Process method. The root cause is the complicated and manual process. Therefore, the chosen solution, with 67.2% result, is to build a systemized tool called The Integrated Assistance Tools. The implementation solution is predicted to decrease by 82.86% of overpayment retirement benefit after a customer passed away during the closing account process or about 3.79% of the total realized operational loss in Bank ABC per year. The implementation of this proposed process is targeted to be ready for use in the third week of May 2024.

Keywords

Operational Loss

Banking Industry

Overpayment Pension Benefits

Service Blueprint

Theory of Constraint (ToC)

Analytical Hierarchy Process (AHP)

INTRODUCTION

Operational loss is a financial loss caused by internal process discrepancies, human (officer) errors, system failures, or other events that affect bank operational activities. The Banking sector is particularly susceptible to operational risk due to its complexity, its dependence on technology, and the variety of activities it undertakes.

As one of the banks that provides pension benefit payments, Bank ABC is exposed to the potential for excess/mistakes in payment of pension benefits. Pension benefits which are state money should be paid appropriately. However, there are sort of conditions when these overpayments are inevitable. The bank as a payment partner is obligated by a cooperation agreement to return the invoiced funds to the pension fund managers within seven working days. Thus, if there is no refund from the heirs, the overpayment will be booked by the bank as an operational loss.

Based on internal data of Bank ABC for FY 2022, the bank recorded operational losses (excluding fraud) 2.4 billion rupiahs or 0.13% from its net income. Management has made efforts to reduce risk events, especially those that impact financial losses. The steps taken are providing coaching and formal punishment in the form of warning letters to every officer who contributes to operational loss.

Therefore, imposing sanctions on officers without further examining the real root of the problem is not only inappropriate in improving the quality of process but also can cause some negative effects to employees and indirectly the company. Based on Bugdol and Puciato [1], the consequences of the received punishment are that the employee felt injustice, lack of motivation to work, dissatisfaction, unwillingness to propose improvement initiatives, etc.

The aims of this research are to:

To identify the most influential key factors/ contribute a large proportion of the overall operational loss at bank ABC

To find out the root cause of operational loss at bank ABC

To provide recommendations for solutions to be able to reduce the nominal operational loss at bank ABC in accordance with the key factors that have been identified previously

This research is focusing on the operational loss of Bank ABC within the financial year 2022. It excludes the fraud factor both internal and external. This research will specifically address one of the activities that most contributed to operational losses at ABC Bank and still has no improvement yet. Furthermore, the operational loss referred to in this research is operational loss outside of internal and external fraud.

Literature review

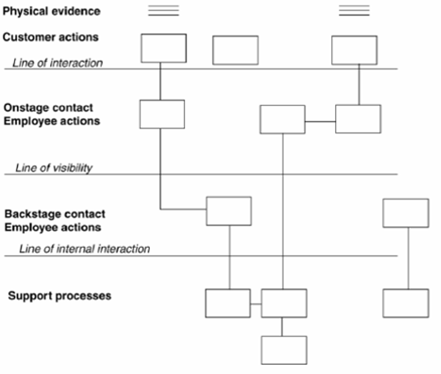

Since services are ethereal and challenging to describe and convey, a service blueprint is essential to the design of a service process [2]. An integrated service delivery structure that meets stakeholder expectations is necessary for the effective and sufficient management of sustainable banking strategy and policy [3].

Service blueprint facilitates the ability of all personnel within the organization to conceptualize a complete service and its progression [3]. Service blueprinting is a methodical approach to assist in managing the customer experience and achieving both customer and company goals [4].

Three phases of development can be distinguished, divided by lines, with regard to the many uses of blueprinting in recent years [5]:

Line of Interaction: Divides the action areas of the supplier and the client. Customers' decisions, behaviors, needs, and interactions are located above this line

Line of Visibility: discern between customer-visible and invisible actions. The "On-stage" interaction and Front Office staff actions are located above this line

Line of Internal Interaction: Delineates actions that take place in the front and back offices. The acts of the staff and the "Backstage" contact are located above this line

Support Processes: those that are performed below the level of internal contact yet are essential to providing the service

A comprehensive service blueprint allows management to assess potential process flaws across the board and execute or enhance a service design [6]. The Service Blueprint offers valuable insights for rethinking the service process and assists in locating and mitigating service failure areas [7].

Figure 1: Representation of Service Blueprint [5]

MATERIALS AND METHODS

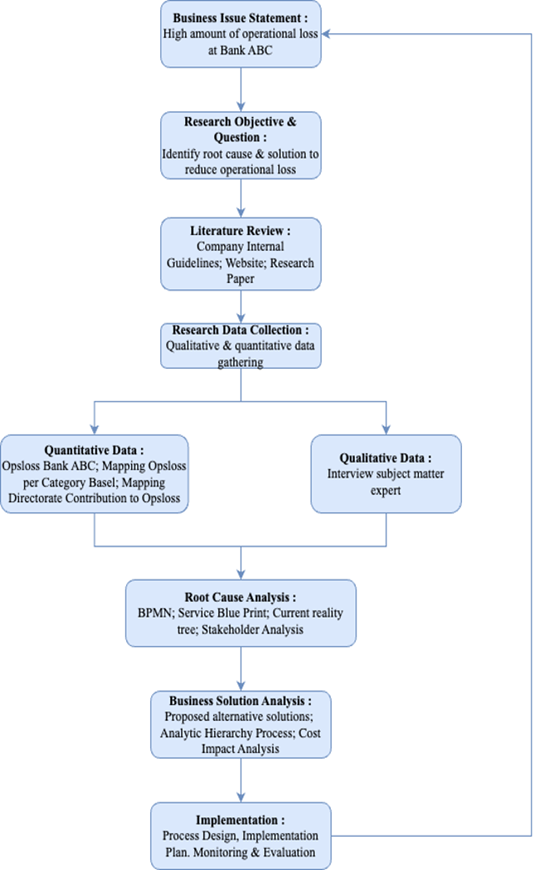

This study combines both qualitative and quantitative methods. As shown in figure 2, after the business issues are identified in the first chapter, then the problem statement, objectives and research questions are formulated. Furthermore, the analysis will be started using the quantitative data from internal banks.

In the next analysis phase, a qualitative analysis is carried out by conducting an in-depth interview with a subject matter expert (SME). The outcome of the interview is the main process / event that contributes the most to the operational loss, which is called the key factor.

The key factors will be analyzed in more depth by using business process modeling notation (BPMN) and service blueprint (Poka-Yoke) to obtain the failure of the process and stage to be improved.

At the business solution stage, the alternative solution will be chosen using analytical hierarchy process (AHP) to then be continued by formulating an implementation plan, including the process controlled by a set of timelines.

Figure 2: Research Methodology

RESULTS

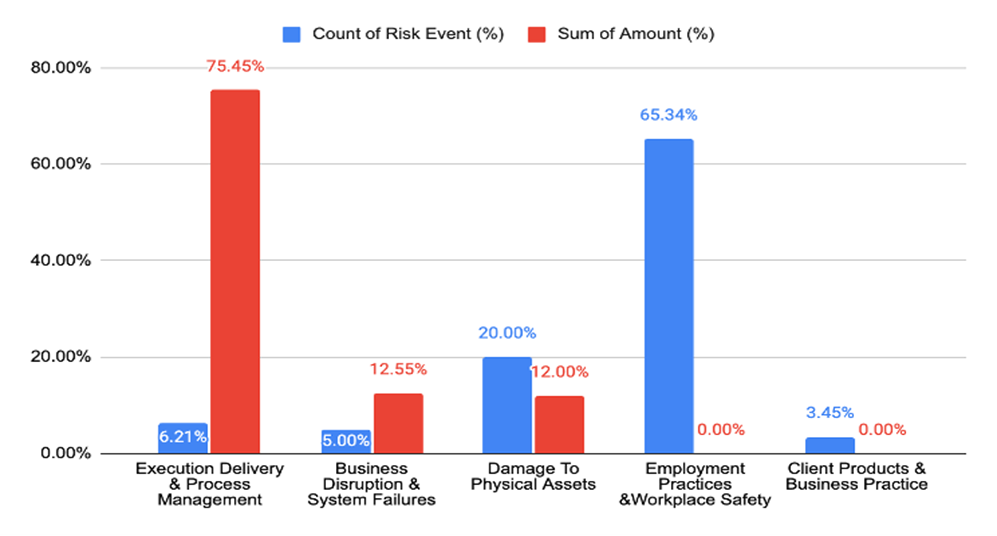

According to internal data of Bank ABC, the execution delivery & process management contributes to almost 80% of total realized operational loss in 2022. Based on in-depth interviews, it was found that the main contributor was the case of excess payments of pension benefits to the heirs of pensioners who had passed away.

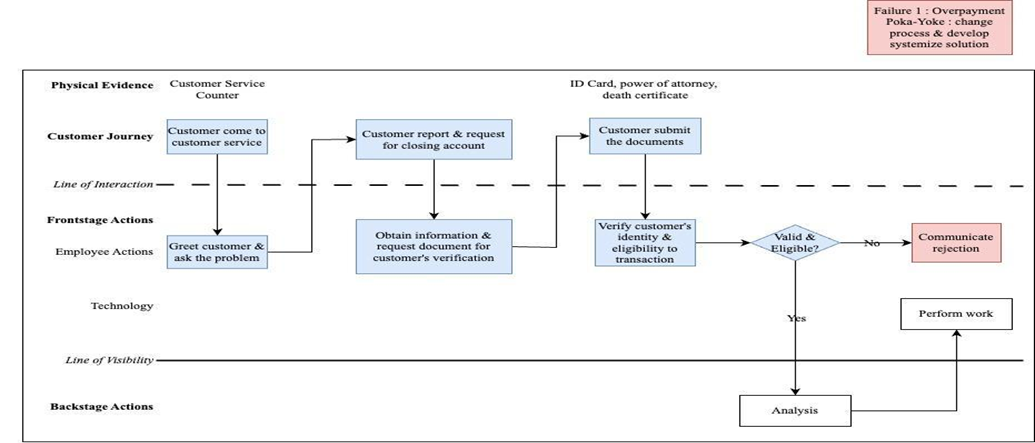

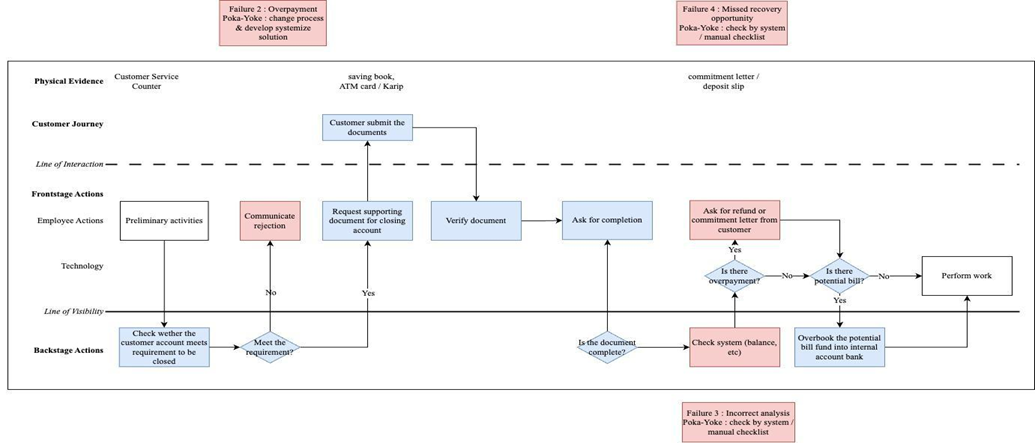

In the process of reporting a pensioner's death, there are failures that need to be detected so that a solution can then be overcome. To achieve increased product quality, the customer journey is depicted using a service blueprint. This is used to help us look at every stage that the customer goes through and what is carried out by bank ABC’s officers as the service provider.

At the preliminary activities stage, as shown in figure 4, there are process weaknesses and potential mistakes that result in operational losses. If the account cannot be closed at the first opportunity upon receipt of information about the pensioner's death, there will be potential losses as follows:

Potential cash withdrawal via teller counter in another branch. The pensioner's heirs may withdraw funds via a teller counter at another branch because the report that the pensioner has passed away is not input into the system and there is no warning if there are future transactions on the pensioner's account. This can be prevented if there is a warning from the system that appears if in the future there is a transaction involving a pensioner's account and because it has been systemized, it will appear wherever the person concerned makes the transaction

The facilities attached to the account, the ATM card, can still be used by other parties to withdraw funds via an ATM machine if they know the pensioner's

ATM card personal identification number (PIN). In many cases, heirs (children or spouses) or close relatives know the pensioner's ATM card PIN because pensioners used to ask for help to withdraw funds via an ATM machine. The current existing process still places ATM card deactivation as part of the account closing process, so that if the account closure requirements are not met on the same day, then all facilities have not been closed. The ATM card facility should be deactivated immediately when a report is received that the pensioner has passed away, regardless of whether the account meets the requirements to be closed at that time or not

Overpayment of legacy funds via teller's counter due to miscalculation in teller (potential of overpayment to customer since teller isn't equipped with tools / access / knowledge to analyze remaining balance of pensioner, while customer service has no obligation to conduct analysis since the closing account is held)

In Figure 5, the analysis stage is the most crucial stage but there are still process weaknesses and quite large potential losses, namely:

Insufficient information for analysis. In some cases, customers don't come to close accounts immediately after insurance claims are complete while the transaction history more than one year isn't available to customer service in the branch. In some cases, the heirs will come back to close the account after more than a year. This makes it difficult for customer service officers at branches to identify the remaining balance on the pensioner's account because the information available to branch officers only shows one year's transactions. This can be addressed if the

Figure 3: Operational Losses Mapping on Event-Type of Basel Category

Figure 4: Service Blueprint-Preliminary Activities

Figure 5: Service Blueprint-Analysis

Figure 6: Service Blueprint - Perform Work

Figure 7: Service Blueprint-Post Work

Figure 8: Current Reality Tree

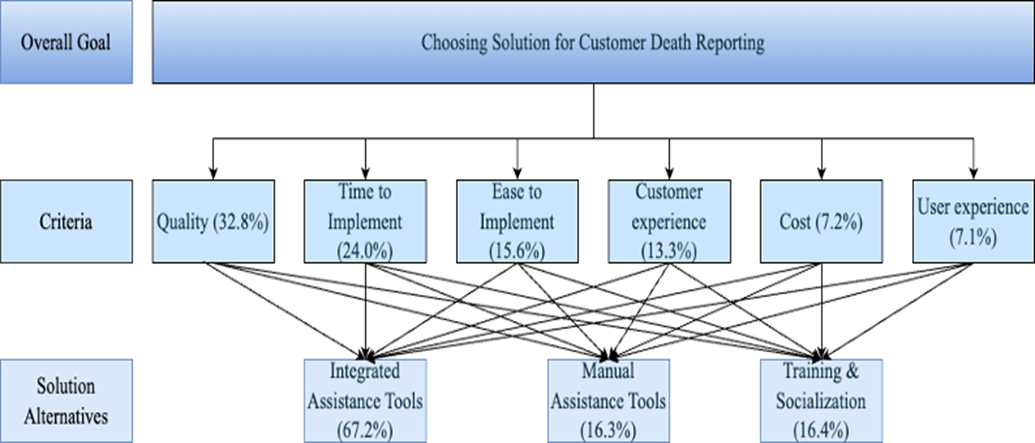

Figure 9: AHP Final Result

identification and analysis process can be carried out by the system, so that there is no need to delay data requests and sacrifice service quality to customers

Inaccurate analysis carried out by customer services regarding balances in pensioner accounts. In some cases, the account may contain pension benefits that are still being received after the pensioner passed away, which does not belong to the pensioner/heirs. This can be overcome by making calculations that were previously manual to be processed with the help of an automatic system

Failed to identify overpayment or potential bill. Withdrawing funds via ATM or teller counter with a power of attorney can be done as long as the pensioner’s account is still active. Among the balances withdrawn may be there’s funds that do not belong to the pensioner/heir. This should be identified by officers at this stage. However, in some cases, officers failed to detect this for various reasons. This can be overcome by making the previously manual analysis process processed with the help of an automatic system

Forgot asking for refund or commitment. Asking customers to return overpaid funds to the bank is a necessity but it is not explicitly written in the technical instructions. However, with manual processes and the absence of technical guidelines, this process is very dependent on the ability of the officers, especially customer service. This can be overcome by making each step of this process can be carried out in a system or at least there is a checklist as a helping tool for officers to ensure that no steps are missed

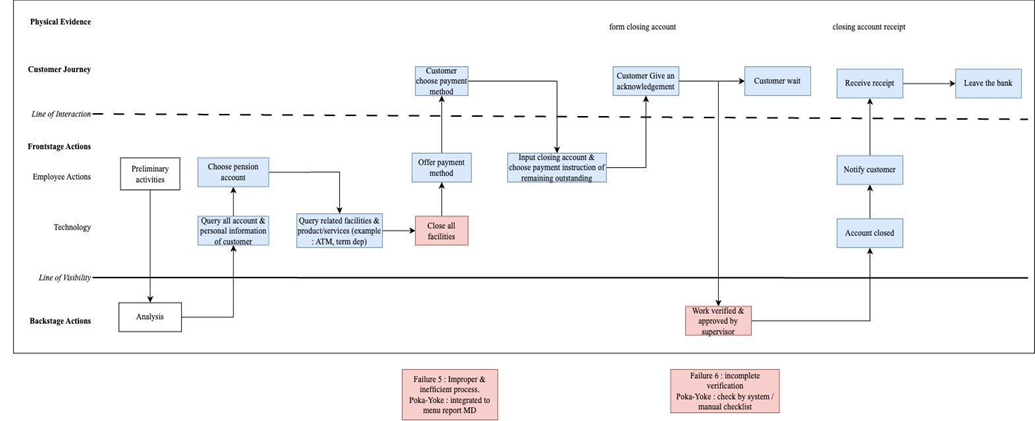

Figure 6 shows the performance work stage, where account closure will be processed. The weaknesses at this stage are:

Special for this type of account, the facility should be deactivated immediately when the pensioner has passed away (even before the pensioner's account is closed) to prevent potential misuse

Supervisor only validates work at the system. To ensure there is dual control in this process, it is necessary to make it compulsory for each stage to get the verification and approval from the supervisor

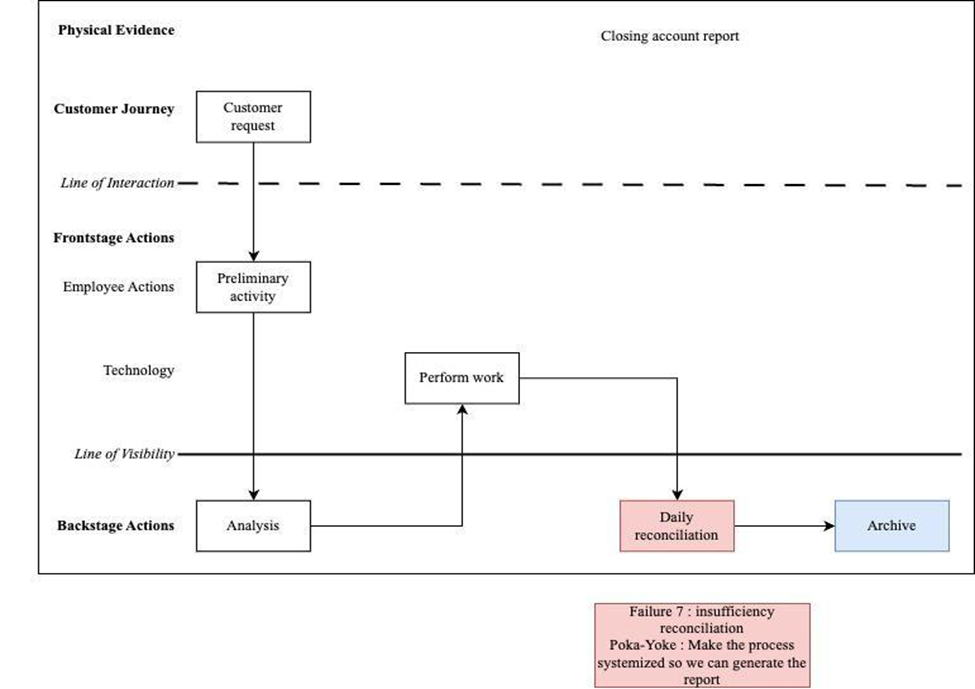

Figure 7 above is a post work stage where there is a process weakness where daily reconciliation is only facilitated for the perform work stage. Meanwhile, the previous stage, especially the analysis, which is more crucial, is not facilitated because the entire process is carried out manually and with single control by customer service itself.

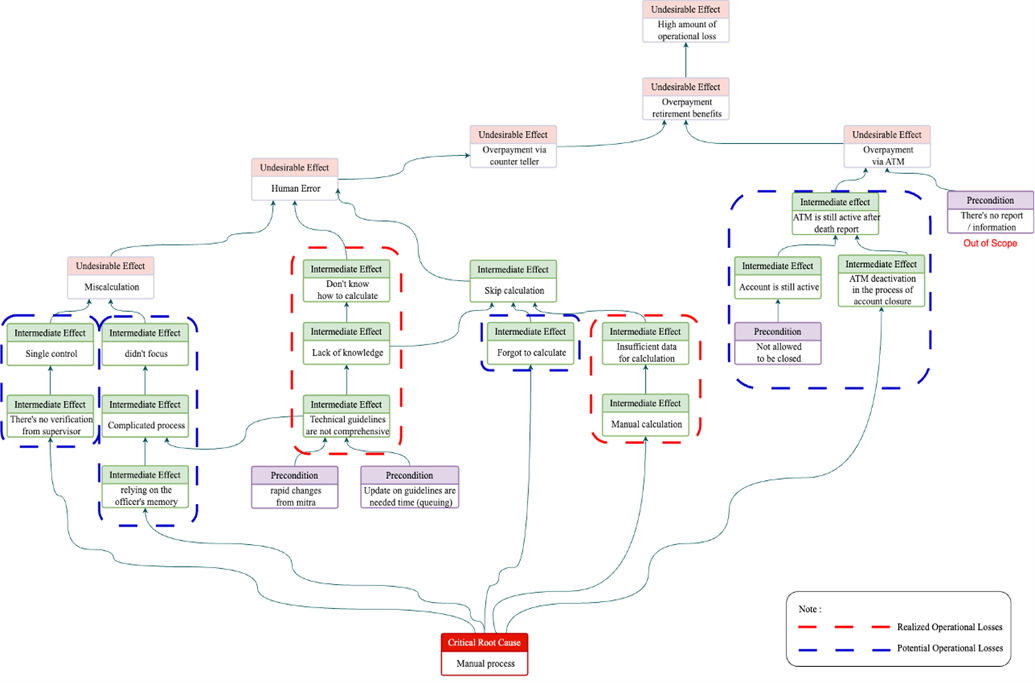

Root cause analysis in this research uses logic current reality tree (CRT), as in Figure 8. All these intermediate and undesirable effects are caused by critical root causes that manual processes. The main solution is to build a systemized tool to overcome the critical root cause. This solution is able to address all failures identified in the service blueprint. However, it needs time and is quite costly. For this reason, the author offers alternative solutions that decision makers can consider which may be less costly and require less time to be implemented. It should be noted that the alternative solutions offered do not answer several problems which could potentially result in potential mistakes that could result in losses.

Based on the judgment of respondents using pairwise comparison, the overall results of proposed alternative solutions are illustrated in the Figure 9. From the result of criteria, it was found that quality (32.8%) was the main consideration for decision makers in determining solutions, followed by time to implement (24.0%), ease to implement (15.6%), and customer experience (13.3%). Meanwhile, cost (7.2%) and user experience (7.2%) are not given much weight in determining the solution.

While from the result of the solution alternative, it was found that Integrated Assistance Tools were the dominant solution chosen, namely 67.2% compared to other alternative solutions, namely Manual Assistance Tools with results of 16.3% and Training & Socialization with results of 16.4%.

CONCLUSION

Based on the business issue faced by Bank ABC regarding the sizable operational loss recorded every year. After deeper dissection, most of operational loss at bank ABC is contributed by execution delivery & process management category (75.45%), with Operations directorate contributing the biggest chunks to operational loss, particularly in Branch Banking Division. Of course, there are several activities / processes that contribute, but the most contributing cases, namely overpayment retirement benefit after a customer passed away during the closing account process is a risk event that has not been resolved and still occurs routinely today. At the end of 2022, the total recorded loss from the process was 4.58% of the total operational loss at Bank ABC while the total operational loss was 0.13% from net income of Bank ABC.

The cause of losses arising from this process is the existence of weaknesses in operational processes that are carried out manually. This complicated and manual process makes frontline officers, especially customer service, the sole determinant in ensuring the accuracy of transactions and all related processes. For this reason, through an analytical hierarchy process with respondents from the branch banking division as decision makers, in this case, they determined a solution to build integrated assistance tools.

Integrated assistance tools are tools that are integrated into the system used by frontline officers at Bank ABC. By implementing this solution, it is estimated that operational loss can be reduced by 82.86% of overpayment retirement benefit after a customer passed away during the closing account process. Or by 3.79% of the total realized operational loss in Bank ABC. The implementation of this proposed process is targeted to be ready for use in the third week of May 2024.

Recommendation

The following are the recommendations that the author gives to Bank ABC or future research:

This research is devoted to the impact in the form of financial losses, it is also necessary to study other impacts that could occur such as reputation risk, compliance, and others

This research is limited to five Basel categories (non-fraud factors), research can be developed into seven Basel categories (including internal and external fraud)

This framework can be carried out on an ongoing basis to reduce operational loss in other processes / activities

REFERENCE

Bugdol M et al. "Punishment of employees–its causes, types, and consequences, as well as factors determining punishment for poor quality." International journal of contemporary management, 2023.

Abdul FW et al. "Improving service quality of call center using DMAIC method and service blueprint." Manajemen dan bisnis, vol. 15, no. 1, 2018.

Tan LH et al. "Service quality implementation in shaping sustainable banking operating system: a case study of Maybank Group." Qualitative research in financial markets, vol. 9, no. 4, 2017, pp. 359-81.

Kazemzadeh Y et al. "A conceptual comparison of service blueprinting and business process modeling notation (BPMN)." Asian social science, vol. 11, no. 12, 2015, pp. 307-18.

Boughnim N et al. "Executive summary using blueprinting method for developing product-service systems." Proceedings ICED 05, the 15th international conference on engineering design, Melbourne, Australia, 15-18 Aug. 2005.

Lee CH et al. "Service design for intelligent parking based on theory of inventive problem solving and service blueprint." Advanced engineering informatics, vol. 29, no. 3, 2015, pp. 295-306.

Nurhidayati N et al. "Business process improvement using service blueprint method on sharia account opening PT Bank Syariah XYZ." Proceedings of the 1st international conference on Islam, science and technology, ICONISTECH 2019, 11-12 July 2019, Bandung, Indonesia, 2021.

None

None

License

Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International License

All papers should be submitted electronically. All submitted manuscripts must be original work that is not under submission at another journal or under consideration for publication in another form, such as a monograph or chapter of a book. Authors of submitted papers are obligated not to submit their paper for publication elsewhere until an editorial decision is rendered on their submission. Further, authors of accepted papers are prohibited from publishing the results in other publications that appear before the paper is published in the Journal unless they receive approval for doing so from the Editor-In-Chief.

Himalayan Journal of Economics and Business Management open access articles are licensed under a Creative Commons Attribution-Share A like 4.0 International License. This license lets the audience to give appropriate credit, provide a link to the license, and indicate if changes were made and if they remix, transform, or build upon the material, they must distribute contributions under the same license as the original.

Advertisement

Recommended Articles

Research Article

Modelling Structure Job Quality, Job Design and Job Satisfaction

Moch Nurhadi,

...

Avi Sunani

Published: 30/08/2022

Download PDF

Cite

x

APA

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. & Sunani, A. (2022). Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management, 3(2), 1-4.

MLA

Nurhadi, Moch, et al. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3.2 (2022): 1-4.

Chicago

Nurhadi, Moch, Moch Bisyri Effendi, Achmad Saiful Ulum and Avi Sunani. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3, no. 2 (2022): 1-4.

Harvard

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. and Sunani, A. (2022) 'Modelling Structure Job Quality, Job Design and Job Satisfaction' Himalayan Journal of Economics and Business Management 3(2), pp. 1-4.

Vancouver

Nurhadi M, Bisyri Effendi M, Saiful Ulum A, Sunani A. Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management. 2022 Jul;3(2):1-4.

Download PDF

Research Article

Accountability and Transparency of Village Fund Management in Lumajang District

Nurina Ayuningtiyas,

...

Muhammad Miqdad

Published: 28/12/2023

Download PDF

Cite

x

APA

Ayuningtiyas, N., Santosa Putra, H. & Miqdad, M. (2023). Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management, 4(2), 1-4.

MLA

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4.2 (2023): 1-4.

Chicago

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4, no. 2 (2023): 1-4.

Harvard

Ayuningtiyas, N., Santosa Putra, H. and Miqdad, M. (2023) 'Accountability and Transparency of Village Fund Management in Lumajang District' Himalayan Journal of Economics and Business Management 4(2), pp. 1-4.

Vancouver

Ayuningtiyas N, Santosa Putra H, Miqdad M. Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management. 2023 Jul;4(2):1-4.

Download PDF

Research Article

Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue

Alfarisy, K. A.,

Wandebori, H.

Published: 30/04/2024

Download PDF

Cite

x

APA

K. A., A. & H., W. (2024). Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue. Himalayan Journal of Economics and Business Management, 5(1), 1-18.

MLA

K. A., Alfarisy, and Wandebori, H.. "Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue." Himalayan Journal of Economics and Business Management 5.1 (2024): 1-18.

Chicago

K. A., Alfarisy, and Wandebori, H.. "Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue." Himalayan Journal of Economics and Business Management 5, no. 1 (2024): 1-18.

Harvard

K. A., A. and H., W. (2024) 'Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue' Himalayan Journal of Economics and Business Management 5(1), pp. 1-18.

Vancouver

K. A. A, H. W. Proposed Digital Marketing Strategy to Enhance Engineering Consultancy Company Revenue. Himalayan Journal of Economics and Business Management. 2024 Jan;5(1):1-18.

Download PDF

Research Article

The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation

Hussein Kamel Wadaa

Published: 05/05/2025

Download PDF

Cite

x

APA

Wadaa, H. K. (2025). The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation. Himalayan Journal of Economics and Business Management, 6(1), 1-10.

MLA

Wadaa, Hussein Kamel. "The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation." Himalayan Journal of Economics and Business Management 6.1 (2025): 1-10.

Chicago

Wadaa, Hussein Kamel. "The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation." Himalayan Journal of Economics and Business Management 6, no. 1 (2025): 1-10.

Harvard

Wadaa, H. K. (2025) 'The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation' Himalayan Journal of Economics and Business Management 6(1), pp. 1-10.

Vancouver

Wadaa HK. The Constitutional and Legislative Basis for Considering the Taxable Capacity of Taxpayers in Iraqi Tax Legislation. Himalayan Journal of Economics and Business Management. 2025 Jan;6(1):1-10.

Amri, A. E. & Utama, A. A. (2024). Analysis of Factors Causing Operational Loss at the Bank Abc to Improve the Bank Financial Performance. Himalayan Journal of Economics and Business Management, 5(1), 1-7.

MLA

Amri, Andi E. and Akbar A. Utama. "Analysis of Factors Causing Operational Loss at the Bank Abc to Improve the Bank Financial Performance." Himalayan Journal of Economics and Business Management 5.1 (2024): 1-7.

Chicago

Amri, Andi E. and Akbar A. Utama. "Analysis of Factors Causing Operational Loss at the Bank Abc to Improve the Bank Financial Performance." Himalayan Journal of Economics and Business Management 5, no. 1 (2024): 1-7.

Harvard

Amri, A. E. and Utama, A. A. (2024) 'Analysis of Factors Causing Operational Loss at the Bank Abc to Improve the Bank Financial Performance' Himalayan Journal of Economics and Business Management 5(1), pp. 1-7.

Vancouver

Amri AE, Utama AA. Analysis of Factors Causing Operational Loss at the Bank Abc to Improve the Bank Financial Performance. Himalayan Journal of Economics and Business Management. 2024 Jan;5(1):1-7.