Keeping engagement high between the bank and its customers proved to be a huge challenge for Rosemary, a digital bank based in Indonesia. Active rate as one of the key metrics within the bank has suffered and dropped significantly over the years. The existing initiatives to keep the engagement are mostly through financial benefits which tends to be effective in the short term but causes significant hit to the cost the bank must bear. There are needs to ensure high engagement from the users, as well as to reach sustainability for the business. One of the main challenges is on how to keep the balance between retaining customers as well as ensuring the business achieves its goals to profitability. In this research, a new Loyalty Program focused on organically engaging Users is proposed. The program should encourage user’s activity by giving them systematic rewards without causing the business to bleed due to the incurred cost. The writer also proposed a change to the usual Loyalty Program framework which mostly did not consider business strategy when initially designed. The proposed Loyalty Program would have several mechanics such as Tiering or Leveling, Point Systems, as well as non-monetary rewards such as Badges. When implemented, the proposed Loyalty Program is expected to increase user’s longevity within the bank as well as boost the bank profitability.

Keywords

Digital Bank

Loyalty Program

Active Rate

Introduction

Full-fledged digital bank has been around since the early 2010s. In the USA and Europe, banks such as Revolut, Chime, Nubank, and Cashapp were launched. These banks utilize mobile applications on Android and iOS (Apple) operating systems to deliver their various banking features to Customers. The idea was simple; digitalizing conventional banking processes to give seamless, faster, and more omnichannel banking experience. Indonesia got its first taste in 2016 with the launching of the first digital bank, Jenius. By 2023, there will be more than 10 Digital Banks that have entered the market. Some of the more well-known names includes; Blu by BCA, Seabank, Bank Jago, and Bank Neo Commerce (BNC).

Before the Digital Banking era, we have been exposed to the Mobile Banking era (2000s – early 2010s). This Mobile Banking era is filled with “Traditional Banks with Online Features” [1]. One example of these is the well-known BCA Mobile. Soon after, a new era of Pseudo digital bank, a set of online banking products being offered from the bank’s Mobile Banking, rises. Few examples of these are PermataMe by Bank Permata and Nyala by OCBC NISP. The advancement of technology and changing customer behavior soon led to the aforementioned launch of the first Digital Bank in Indonesia.

In 2016, the younger generation (Millennials at that time), dominated the Digital Bank takers or Users. This younger generation are much more well equipped to understand such a novel product that is Digital Bank. When the pandemic strikes in 2019/2020, people will be forced to work from home and limit their mobility. Every daily task, including banking, was limited. During this time, the acquisition and adoption for digital products accelerated significantly, and this would include Digital Bank adoption. As of now, while most Digital Bank users are still on the younger side (< 35 years old), many more Users are coming from the older age brackets.

In Indonesia, the internet adoption rate has also grown significantly in the past several years. The internet penetration rate in Indonesia for 2023 is around 66% [2]. In 2022, that number stands at 62%, which means there is a significant increase year on year. Across the past five years, the number has doubled. Digital banksrely on two things, Device (smartphone) and Internet Connection. Indonesia’s internet penetration has been growing steadily in the last 10 years. From the demographic profile, Indonesia’s bonus demography will also push the Digital Bank adoption further. In 2021, Around 78% Indonesians have at least used digital banking actively, either via mobile or online channel [3].

Even though the numbers look good on the Digital Banking market, the actual habit of Indonesians towards the product proves challenging for the business to reach profitability. The most challenging part is that people are still very price sensitive. Research also reveals that after the pandemic, people are becoming more price sensitive than ever. [4] The effects of this phenomenon is that people tend to have a low loyalty towards a particular brand or product. This is a very big challenge for digital banks (or banks in general). Banking generally provides the same services and products. The differences are usually in price, experience, and services. Currently, it is safe to say that the cost–of–switching is very low in this market.

Due to the low loyalty behaviour of the market, one particular digital bank which will be the topic of this research, finds it difficult to retain its Users. From 100% users acquired and activated the product, barely two users stayed after a full year. This particular phenomenon will hurt the bank bottom-line as the cost to maintain the users is greater than the profit that the same user brings. Furthermore, the competition is not only coming from digital banks or banks in general. e-Wallets such as GoPay, OVO, Shopee Pay, and DANA have also proven to be competitors for digital banking especially in the payment department. Users generallyfind it easier to register and sign-up for these services rather than to register for a bank account.

This research will focus on how Rosemary (pseudonym for a digital banking in Indonesia) can tackle the Customer Retention issue and the implementation strategy on how to win the market. Several research questions raised are:

What is the main delighter for Customers which makes them stick with using Rosemary

What are the main churn factors when Customer decides to leave Rosemary?

How might we develop a sustainable Loyalty Program to increase Rosemary’s Active Rate?

The theoretical foundation of this research is the Customer Life Cycle theory and how Loyalty Program can contribute to the theory. This theory foundation is crucial for businesses to comprehend as it provides a framework for understanding and managing customer relationships effectively. It can also serve as an analytical tool to understand further how a customer interacts with the brand, as well as how the brand can improve its customer experience.

The customer life cycle generally covers five key stages. These stages would represent the various phases a customer goes through on their relationship with a brand.

The stages of the customer life cycle are as follows:

Reach: This stage involves capturing the attention of potential customers and creating awareness of a company's products or services.

Acquisition: In this stage, the focus is on converting potential customers into paying customers by effectively communicating the value proposition of the products or services.

Conversion: This stage centres on ensuring that the customer has a positive experience with the product or service and is satisfied with their purchase.

Retention: The retention stage involves maintaining the customer's loyalty to the product or service and encouraging them to continue using it. The outcome of the retention stage is usually either Loyalty or Churn.

Loyalty: This final stage is all about nurturing long-term relationships with satisfied customers, who may opt for additional services, higher-priced options, and become advocates for the brand by recommending the products or services to others.

The main topic for this research is about active rate, and in the Customer Life Cycle theory, it correlates heavily with the retention phase. During this phase, the brand puts a lot of effort into keeping a Customer happy and sticks with using the products. This phase can be costly if mismanaged as it can lead to inefficiency and customer churn. One of the initiatives that brands use is the Loyalty Program.

Loyalty programs can be defined as a spectrum of marketing initiatives, varying from promotional gifts, points accumulation, customer levels and/or other means with the goal of influencing customer behavior towards the brand [5]. Many brands both in Indonesia or globally have employed Loyalty Program as their strategy to retain customers as long as possible. In the dynamic landscape of Indonesia's business environment, numerous tech-based companies, including but not limited to Gojek, Tokopedia, and Dana, have successfully implemented loyalty programs. This trend is not exclusive to the tech sector, as banks have also ventured into loyalty programs, both in digital and non-digital realms. While the digital side of the market has witnessed innovative approaches to loyalty initiatives, non-digital programs often leverage offline sales channels for program communication and execution. This multifaceted engagement with loyalty programs reflects a broader industry acknowledgment of the strategic significance of customer retention and engagement across diverse sectors in the Indonesian market.

I.1 Loyalty Program and its Value towards Business/Brands

The ultimate goal of Loyalty Program is to encourage repeat purchases, increase customer’s spending and to capture a bigger share of customer’s wallet [6]. One of the importance of customer loyalty is that it can provide sustainability for companies in customer attraction and retention [7]. Competitive value and advantages are another result of achieving Customer Loyalty according to the same researchers.

Another research stated that the Loyalty Program could have an instant positive impact but proved unsustainable in the long run [8]. It was important to note that the research used a brick-and-mortar business as the main research subject with category sales and profitability as the metric assessed. Different results might apply when we use digital business or brands and different outcome metrics as the main subject.

Other interesting findings about Loyalty Program came from which discussed how businesses might be building the wrong program mechanics. The researchers stated that the most common Loyalty Programs use points as the main attraction points for Customers. When these points’ value are higher than the fair market value, Customers tend to get upset, disinterested, and eventually disregard the Loyalty Program at all [9].

It is also discovered that the effectiveness of loyalty programs has been inconclusive regarding their worth. It was also suggested that a narrow focus on the financial rewards of loyalty programs is one reason for their failure to maintain customers long-term, and that future research should emphasize non-financial benefits, such as status, habits, and relationships. Research has identified customer-company identification (CCID) as an effective sociological mechanism through which loyalty programs can build and maintain relationship-based customer loyalty [10]. This mechanism provides a natural overlap of the gaps in CCID research and the need for more focused research on the benefits of loyalty programs. In the context of loyalty programs, non-financial benefits provide customers with a basis for developing a deeper relationship and identity with the company, specifically, CCID.

The same literature also suggests that loyalty programs are an important marketing instrument used to promote repeat purchases and customer relationships. The most common benefits of implementing loyalty programs for providers include an increase in the company's reputation and profits [11] (Alshurideh, Al-Gasaymeh, Ahmed, & Alzoubi, 2020). However, the effectiveness of loyalty programs depends largely on proper customization of all program elements, and the degree to which a scheme fulfills a set of clearly outlined objectives (Chen, Mandler, & Meyer-Waarden, 2021) [12].

From these research we can learn that building a Loyalty Program needs to be Customer centric to be sustainable and lovable by Customers. All in all, how businesses build Loyalty Programs should depend on the industry and the demographic & behaviour of their customers [4]. There is no one size fits all approach to design the most suitable Loyalty Programs to yield positive results.

I.2 Loyalty Program Components

In order for a Loyalty Program to work effectively, it has to have several components working together. Multiple sources of information have been gathered and visualized on the table below.

Table 1. Loyalty Program Components, a compilation of studies

Components

Description

Reward System

Incentives for customers, be it monetary or non-monetary

Customer Centric Approach

Addressing customer needs in order to forge emotional connection to the brand

Personalization

A customized approach for specific customers

Brand Relation/Identity

A tailored program which reflects the personality of the brand and be an extension of the brand

Communication Channels

Ways of communicating the program to the Customers (e.g. via apps, brochure, sales agent)

Gamification Elements

Incorporation of game-like features and mechanics to influence customer to do certain activities

I.3 Integrating the Loyalty program Elements with Business Perspective

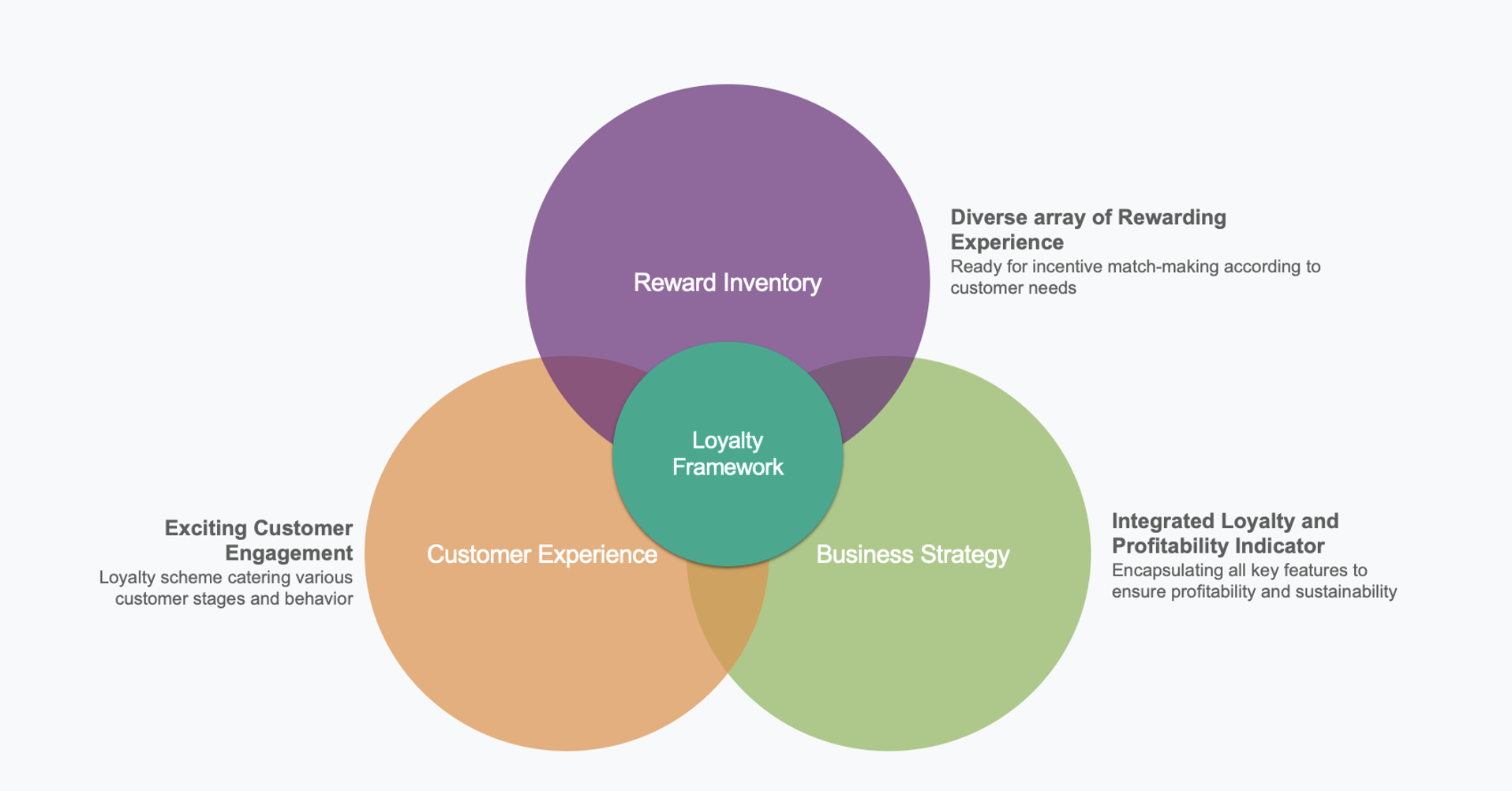

From the Loyalty Program elements theory, the writer will group the components into three big items that can be easily visualized. The writer will call this framework the Loyalty Framework. Inside the framework there are three big building blocks which integrate loyalty program elements on the table above with business perspective. The three building blocks are Rewarding Experience, Business Profitability, and Customer Experience.

Figure 1. Loyalty Program Framework

Reward Inventory

Loyalty programs and rewards cannot be separated as it is the main tool to incentivize user’s action. Previous research discovered that combination of reward types (inventories) as well as reward issuance timing could influence the loyalty of customers. Monetary and non-monetary rewards for a Loyalty Program should be considered to create a balance between customer loyalty and business profitability.

The rewarding experience is also a crucial item to consider as it might be perceived differently by each user. Giving a reward too late or too sparsely might hinder users from creating continuous engagement with the brand [4].

Customer Experience

Customers tend to connect more with brands that provide exciting experiences. When creating Loyalty Programs, the customer's experience plays a crucial role in determining their satisfaction and engagement with the program. This is especially important in the banking industry, where many products are similar. A positive customer experience becomes a unique selling point for banking products, helping them stay competitive in the market [13].

A well-designed Loyalty Program should be straightforward and appeal to a broad range of customers. To achieve this, the designer needs to consider users' habits and usage patterns. Additionally, it's important to be careful when designing the program to avoid giving out too many rewards or doing so too frequently, as this can impact the profitability of the business. Striking the right balance in the program design is essential for keeping customers engaged while ensuring the business remains financially sustainable.

Business Strategy

The general aim of the business when introducing a Loyalty Program is to increase their customer’s retention rate (or active rate). This in turn is expected to drive more sales, increase engagement, and eventually turn the customer into brand advocate/ambassadors. All of this will contribute to more profitability to the business. In conclusion, a Loyalty Program should have business strategy and goals incorporated. When designing a Loyalty Program, the end-in-mind should always be the business, although a balance with the other two building blocks within the Loyalty Program Frameworks should be achieved.

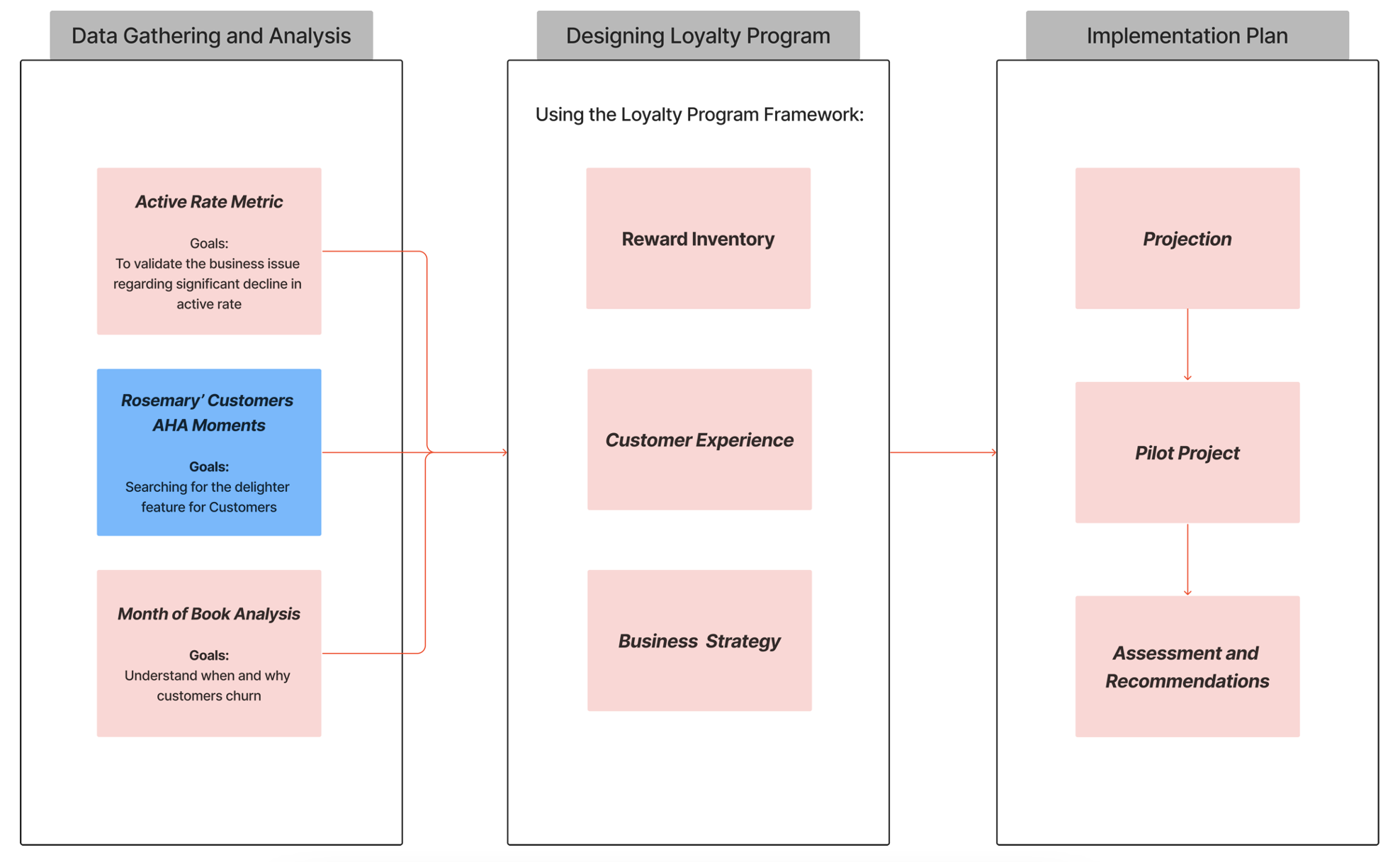

I.4 Research Design

The overall design for this research will be divided into three stages. Stage 1 is for Data Gathering and Analysis. Stage 2 is to focus on Designing the Loyalty Program. The last stage is to do the implementation of the proposed loyalty program, including to give assessment and recommendation for the business.

Figure 1. Loyalty Program Framework

In the three stages mentioned above, both quantitative and qualitative data will be collected, but the analysis will mainly focus on qualitative analysis as this research aims to propose the concept and design of Loyalty Program.

Results & Discussion

II.1 Rosemary’s Customer Behavior

Based on primary data gathering and analysis, it was determined that Rosemary’s customer likes several features from Rosemary. The features with the highest usage and appreciation from users are saving products, card products, and QR payment. Furthermore, the customers are also identifying foreign currency, lending, investments, and time deposits products as a delighter feature. These delighter features are described as features that they like but still rarely use.

Based on the yearly Net Promoter Score (NPS), around 41% of all respondents say that they are willing to promote Rosemary to others. It was clear that the top reasons why Users use Rosemary is due to the product variations available. All three groups of banking products (saving, lending, transactions) are mentioned in the survey as one of the main attractors of using Rosemary. Easiness of international transaction also mentioned by Users as the attractor for them to promote rosemary to others. One interesting thing to note is that users still say that good promotions and free transactions are something that attracts them as well. This might indicate that some users felt that their relationship with the brand is merely transactional.

As for the rest of the survey population, they belong to the passive promoters and detractors. Meaning, they are not actively promoting Rosemary, or even worse, influencing others to not use Rosemary products. The main reasons are because these users feel that Rosemary’s app performance is not satisfactory and because the monthly administration fee is not worth the price versus what they currently receive. Meaning, there are gaps between the user's expectations of Rosemary’s value versus what they actually get. One interesting thing to note is that users also mentioned that they feel Rosemary’s interest rates are less competitive than competitors, and that Rosemary lacks promotion.

II.2Rosemary’s Current Loyalty Program

It is crucial to understand the current Loyalty program performance in Rosemary’s business. Rosemary has a form of Loyalty Program feature inside the digital-app. It is a tier-based program which offers more benefits towards certain customers. Currently, the tiers are based on a single-metric system which considers Customer’s funding balance in Rosemary. The higher the funding balance, the higher the level will be. Generally, free transaction and free cash withdrawal quota are given as the default reward type. The rewards that customers will receive on certain tiers are differentiated by the number of rewards.

This current scheme does not drive loyalty from the customers towards the brands. It was very saturated at Tier-1 which indirectly indicates that users are not motivated to reach the next tiers or that the requirements are deemed too difficult by users. For a Loyalty Program to works, there are several components which has to be fulfilled (elaborated on chapter 2 of this research)

Table 2. Rosemary's Loyalty Program Check-up According to Loyalty Program Elements

Components

Rosemary’s Version

Fulfilled by Current Loyalty Program

Reward System

A default reward of transactional and cash withdrawal free quotas which given every start of month

Yes

Customer Centric Approach

No approach to fulfil and match user’s habit and needs

No

Personalization

Same standardized system and program for all users. Differentiated only on number of reward given emotional connection to the brand

No

Brand Relation/Identity

Current loyalty program speaks Rosemary. The main key is due to the longevity of this program which has been offered since Rosemary launched

Yes

Communication Channels

Current loyalty programs are passively communicated via the Rosemary website and digital app.

Partly

Gamification Elements

No gamification elements within the current loyalty program

No

II.3 Proposed Loyalty Program for Rosemary

According to Negi’s research in 2022 about Loyalty Program in the UK and their effectiveness, there are at least 5 types of Loyalty Program that are commonly found in the market. The 5 types are Monetary Rewards, Point System, Tier System, Upfront Charge for VIP Benefits, and Non-monetary programs/rewards. The research shows that while all types of loyalty programs have positive benefits to user’s engagement and loyalty, Monetary Rewards and Tier System are the top two among the options.

Table 3. Loyalty Program Type based on Negi (2022)

Loyalty Program Type

Researcher Notes

Monetary Rewards

Suitable for acquiring short-term customers; instant results

Tier System

Extracting long-term value of the loyalty program

Point System

Extracting short-term value of the loyalty program

Charge an upfront fee for VIP benefits

Suitable for business which relies on frequent and repeated purchases

Non-monetary programs/rewards

Have positive but the least effective. Might be suitable for certain business types

When considering the business needs of Rosemary to increase active rate for both new joiners and legacy joiners, as well as the needs to ensure sustainability from financial perspectives, then a combination of Tier System, Point System, and Non-monetary Programs/Rewards.

II.3.1 Tier System

Tier System is chosen due to its longevity and long-term focus. Rosemary will aim to stretch User’s usage and lifetime with Rosemary as long as possible so it is going to be suitable to go with this system as the base of the entire Loyalty Program. Point System is chosen to give flexibility to the business in giving financial rewards and induce habit for Users to keep using Rosemary’s products. Non-monetary rewards will balance out all the rewards which have financial impacts such as points and free transactions which are the basic rewards in Rosemary. Non-monetary rewards can also impact the emotional relationship between Users and Rosemary products.

The proposed Loyalty Program will allow Rosemary’s customers to be on a certain level according to their achievements on using Rosemary. We will introduce three methods/metrics for Customers to level-up their tier/levels. This will give flexibility to each customer to find their pattern and habit of using Rosemary. Furthermore, customers can also earn rewards which come after they have done certain activities. The main rewards that will be given are points to encourage long-term sustainable engagement with Rosemary. Lastly, customers can also earn badges which indicates their progress and journey with Rosemary. In the upcoming sections, the proposed loyalty program will be discussed in further details.

The new tiering system will utilize a triple-metric system which rewards all types of users. Generally, there are three types of activities in banking which are Saving, Transacting, or Lending. By using triple metric, we can ensure we incentivize and put every user on equal footing. The metric will be Funding Balance, Transaction Frequency, and Lending Utilization. The triple metric progress will work in parallel, which means users can do their usual/ activities with Rosemary and all the progress will fuel each corresponding progress bar.

When a user frequently uses Rosemary to do transactions, they will be rewarded with this Loyalty Program. The transactions included in this metric are all payment transactions via QRIS, Card Payment, and also digital payment (bills payment) methods. It is proven in the banking industry when User’s transactions are increasing in frequency or volume, then their funding balance will also increase correspondingly. This will further justify the introduction of this second metric as it will create synergy with the funding balance metric as well.

The numbers proposed will ensure transaction profitability for Rosemary in each proposed level. As mentioned previously, not all transactions are counted as a progress for this metric. For example, transfer out to Rosemary or to another bank will not be counted as a progress due to the nature of business.

Table 4. Breakdown of Transactions in Rosemary

Transaction counted as progress

Transaction not counted as progress

QRIS Payment

Bills Payment

Investment Purchases

Card Payment (both Debit and Credit Card)

Transfer to other Rosemary accounts

Transfer to other banks

Overbooking from account to account

Buy and Sell Foreign Currency

The third and final metric will cater to users who like to use Rosemary almost exclusively for the lending products. Rosemary has three lending products which are Credit Card, Unsecured Loan, and Buy Now Pay Later (BNPL). The metric that will be used here is the combined outstanding loan for all lending products.

As lending productsoffer the highest margin and profitability (albeit the higher risk) for the business, the threshold will be quite lenient and easy to achieve for Users. This will also encourage users to take on more loans as the numbers are achievable. Like on transaction metric, the VIP level will not consider this metric for the tier system.

II.3.2 Reward System

The proposed loyalty program will utilize points as the main currency of rewards for Users. Rosemary will cut back the fiat-based cashbacks and discounts in favor of this point currency. These points will be given for Users in certain levels, so it will be tied up with User’s achievement and activities. Aside from points, it was also proposed that Rosemary balanced the reward and incentive by giving social rewards with social donation. The proposed rewards can be seen in detail in the table below, and the usage mechanism of the points will be discussed further in the next section of this research.

Table 5. Proposed Rewards/Incentive for Rosemary Loyalty Program

Reward Type

Level 1

Level 2

Level 3

Level 4

Level VIP

Point Reward

0 Points

150 Points

750 Points

2000 Points

5000 Points

Non-monetary (Social Donation)

-

IDR 2,000 Social Donation

IDR 5,000 Social Donation

IDR 15,000 Social Donation

IDR 30,000 Social Donation

Aside from point rewards, it is also proposed that Rosemary have a badge reward. The aim for the badge (non-monetary rewards) is to balance out the cost that Rosemary has to bear in giving users incentive and rewards. The badges proposed will aim to encourage users to achieve every single badge available. There will be five groups of badges ranging from Registration, Transactions, Funding, Lending, and Product Exploration. Each group will have multiple collectible badges that users can receive after completing certain requirements. The requirements are designed to encourage user’s longevity in using Rosemary. For example, there will be badges to thankusers when they have stayed loyal with Jenius for 5 years and ten years. Furthermore, there will be a special badge reserved for users who have done a total of 100,000 transactions with Rosemary or users who have IDR 100,000,000,000 with Rosemary. These kinds of badges will cater to the most loyal and/or wealthy users in Rosemary, ensuring every kind of usergets appreciated properly. The next iteration of this badge could be tying the badges up with financial rewards such as points and cashbacks as well.

II.4 Expected Business Impact

From the proposed design of the Loyalty Program for Rosemary, it was expected that the overall customer quality and retention would be increased. Looking at the business perspective, there are two predetermined goals to be achieved which is the overall active rate (retention rate) and also the CVI (profitability index). Both metricsneed to go hand-in-hand.

II.4.1 Active Rate

It was expected for the active rate curve to slope easier than the current data. Since this research focuses on retention and not acquisition, the expected outcome would be a shift on the slope angle as illustrated by the chart below (Figure 14.). Reduced sloped would mean lower churn in early months and improvement in retention when Users are going further in time with using Rosemary.

II.4.1Customer Value Index

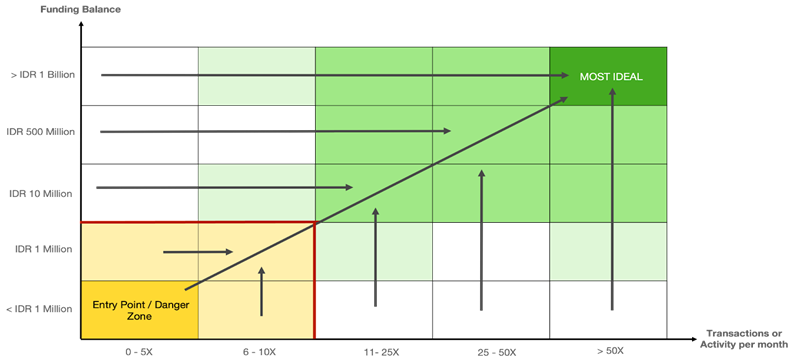

Increasing retention rate would eventually also increase the profitability of the business. The expectation of the proposed loyalty program would be to shift customers to the higher-right of the CVI clustering. The proposed triple-metric tier system and badge rewards would encourage users to do more transactions and to have more funding balance with Rosemary would then shift their position higher in the cluster.

Figure 3. Funding Balance and Transaction Activity impact to CVI

In the chart above, we can see that it is the business’ expectation to have Customers who use Rosemary’s product for both saving and also transactional activities. We would expect these users to do organic activities within Rosemary to step up into the nearest ideal cluster spot with an indirect push from the proposed loyalty program.

Conclusion

Rosemary customers churn significantly in the first 3 months, then still churning the longer they were using Rosemary’s products. The main reason why customers leave is due to a gap between Rosemary’s product and their expectations. Customers still feel that the app performance is still unsatisfactory, and that the monthly administration fee is not yet worth it to be paid. On the other hand, it was revealed that Customers like and tend to be more loyal with Rosemary if they found out about the basic and delighter features such as Saving Products, Foreign Currency Account, as well as investment products.

From various researches, it was found that a Loyalty program is composed mainly of 7 elements. The writer of this research proposed a new Loyalty Program framework which integrates business strategy towards the existing loyalty program elements. The framework consists of three building blocks which cater the Reward Inventory, Customer Experience, and Business Strategy.

Considering the existing loyalty program which Rosemary has implemented, as well as the customer behavior, it was decided that the best loyalty program tools for Rosemary is a combination of Tier-system, Point-system, and Non-monetary Rewards. It would be a personalized Loyalty Program which caters all segments. Furthermore, from the business strategy perspective, the loyalty program would be designed to cater two specific business metrics which are active rate and Customer Value Index (CVI).

The proposed Loyalty Program would have a triple-metric system as the means of progression for Users, allowing them to use Rosemary however they like. Rosemary would then incentivize users' activity with points and badges. The points would be used as the primary currency to do all activities in rosemary such as to off-set the transfer fee or to purchase vouchers.

The expected outcome for the business is a shift in both Active Rate metric and CVI metric. For the Active Rate, it is expected that the slope and drop of the trend is much slower than the current rate. For the CVI, it is expected that a shift to the upper right of each cluster for the customers. This means that both the retention and profitability in Rosemary would be expected to increase with the introduction of the proposed loyalty program.

Acknowledgments: The authors would like to appreciate all parties who contributed to the writing of this research.

Author Contributions: All authors contributed equally to the writing of this paper. All authors read and approved the final manuscript.

Conflicts of Interest: There are no conflicts of interest.

Ethical approval: The study was approved by the Institutional Ethics Committee ofInstitut Teknologi Bandung

References

Agarwal, Reeti, Ankit Mehrotra, and Dheeraj Misra. "Customer happiness as a function of perceived loyalty program benefits-A quantile regression approach." Journal of Retailing and Consumer Services 64 (2022): 102770. https://doi.org/10.1016/j.jretconser.2021.102770

Alshurideh, Muhammad, et al. "Loyalty program effectiveness: Theoretical reviews and practical proofs." Uncertain Supply Chain Management 8.3 (2020): 599-612. DOI: 10.5267/j.uscm.2020.2.003

Arbore, Alessandro, and Zachary Estes. "Loyalty program structure and consumers' perceptions of status: Feeling special in a grocery store?." Journal of Retailing and Consumer Services 20.5 (2013): 439-444. https://doi.org/10.1016/j.jretconser.2013.03.002

Çakaloğlu, Mısra. "Customer Experience in the Banking Industry." Handbook of Research on Interdisciplinary Reflections of Contemporary Experiential Marketing Practices. IGI Global, 2022. 383-402. http://dx.doi.org/10.4018/978-1-6684-4380-4.ch018

Chen, Yanyan, Timo Mandler, and Lars Meyer-Waarden. "Three decades of research on loyalty programs: A literature review and future research agenda." Journal of Business Research 124 (2021): 179-197. https://doi.org/10.1016/j.jbusres.2020.11.057

Danaher, Peter J., Laszlo Sajtos, and Tracey S. Danaher. "Does the reward match the effort for loyalty program members?." Journal of Retailing and Consumer Services 32 (2016): 23-31. https://doi.org/10.1016/j.jretconser.2016.05.015

Fourie, Sonja, Michael Goldman, and Michael McCall. "Designing for loyalty programme effectiveness in the financial services industry." Journal of Financial Services Marketing 28.3 (2023): 502-525. https://doi.org/10.1057/s41264-022-00158-9

Henderson, Conor M., Joshua T. Beck, and Robert W. Palmatier. "Review of the theoretical underpinnings of loyalty programs." Journal of consumer psychology 21.3 (2011): 256-276. https://doi.org/10.1016/j.jcps.2011.02.007

Leenheer, Jorna, et al. "Do loyalty programs really enhance behavioral loyalty? An empirical analysis accounting for self-selecting members." International Journal of Research in Marketing 24.1 (2007): 31-47. https://doi.org/10.1016/j.ijresmar.2006.10.005

Lin, Chen, and Douglas Bowman. "The impact of introducing a customer loyalty program on category sales and profitability." Journal of Retailing and Consumer Services 64 (2022): 102769. https://www.sciencedirect.com/science/article/abs/pii/S0969698921003350#:~:text=https%3A//doi.org/10.1016/j.jretconser.2021.102769

McKinsey. "Emerging Markets Leap Forward in Digital Banking Innovation and Adoption." McKinsey, (2021), https://www.mckinsey.com/industries/financial-services/our-insights/emerging-markets-leap-forward-in-digital-banking-innovation-and-adoption.

Momentum Works. "Rise of Digital Banks in Indonesia." Momentum Works, (2021), https://momentum.asia/product/rise-of-digital-banks-in-indonesia/.

World Bank. "Individuals using the Internet (% of population) - Indonesia." World Bank, (2023), https://data.worldbank.org/indicator/IT.NET.USER.ZS?locations=ID.

Advertisement

Recommended Articles

Research Article

Modelling Structure Job Quality, Job Design and Job Satisfaction

Moch Nurhadi,

...

Avi Sunani

Published: 30/08/2022

Download PDF

Cite

x

APA

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. & Sunani, A. (2022). Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management, 3(2), 1-4.

MLA

Nurhadi, Moch, et al. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3.2 (2022): 1-4.

Chicago

Nurhadi, Moch, Moch Bisyri Effendi, Achmad Saiful Ulum and Avi Sunani. "Modelling Structure Job Quality, Job Design and Job Satisfaction." Himalayan Journal of Economics and Business Management 3, no. 2 (2022): 1-4.

Harvard

Nurhadi, M., Bisyri Effendi, M., Saiful Ulum, A. and Sunani, A. (2022) 'Modelling Structure Job Quality, Job Design and Job Satisfaction' Himalayan Journal of Economics and Business Management 3(2), pp. 1-4.

Vancouver

Nurhadi M, Bisyri Effendi M, Saiful Ulum A, Sunani A. Modelling Structure Job Quality, Job Design and Job Satisfaction. Himalayan Journal of Economics and Business Management. 2022 Jul;3(2):1-4.

Download PDF

Research Article

Accountability and Transparency of Village Fund Management in Lumajang District

Nurina Ayuningtiyas,

...

Muhammad Miqdad

Published: 28/12/2023

Download PDF

Cite

x

APA

Ayuningtiyas, N., Santosa Putra, H. & Miqdad, M. (2023). Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management, 4(2), 1-4.

MLA

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4.2 (2023): 1-4.

Chicago

Ayuningtiyas, Nurina, Hendrawan Santosa Putra and Muhammad Miqdad. "Accountability and Transparency of Village Fund Management in Lumajang District." Himalayan Journal of Economics and Business Management 4, no. 2 (2023): 1-4.

Harvard

Ayuningtiyas, N., Santosa Putra, H. and Miqdad, M. (2023) 'Accountability and Transparency of Village Fund Management in Lumajang District' Himalayan Journal of Economics and Business Management 4(2), pp. 1-4.

Vancouver

Ayuningtiyas N, Santosa Putra H, Miqdad M. Accountability and Transparency of Village Fund Management in Lumajang District. Himalayan Journal of Economics and Business Management. 2023 Jul;4(2):1-4.

Download PDF

Research Article

The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable

Fitria Dina Alvina,

...

Taufik Kurrohman

Published: 01/06/2025

Download PDF

Cite

x

APA

Dina Alvina, F., Sayekti, Y. & Kurrohman, T. (2025). The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable. Himalayan Journal of Economics and Business Management, 6(1), 1-5.

MLA

Dina Alvina, Fitria, Yosefa Sayekti and Taufik Kurrohman. "The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable." Himalayan Journal of Economics and Business Management 6.1 (2025): 1-5.

Chicago

Dina Alvina, Fitria, Yosefa Sayekti and Taufik Kurrohman. "The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable." Himalayan Journal of Economics and Business Management 6, no. 1 (2025): 1-5.

Harvard

Dina Alvina, F., Sayekti, Y. and Kurrohman, T. (2025) 'The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable' Himalayan Journal of Economics and Business Management 6(1), pp. 1-5.

Vancouver

Dina Alvina F, Sayekti Y, Kurrohman T. The Influence of Managerial Ownership and Institutional Ownership on Manufacturing Company Value with Corporate Social Responsibility (CSR) as a Moderating Variable. Himalayan Journal of Economics and Business Management. 2025 Jan;6(1):1-5.

Download PDF

Research Article

Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya

Kinisu Sifuna,

...

Peter Simotwo

Published: 30/06/2021

Download PDF

Cite

x

APA

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. & Simotwo, P. (2021). Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management, 2(1), None-None.

MLA

Sifuna, Kinisu, et al. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2.1 (2021): None-None.

Chicago

Sifuna, Kinisu, David W. Lwangale, Peter Simotwo, Kinisu Sifuna, David W. Lwangale and Peter Simotwo. "Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya." Himalayan Journal of Economics and Business Management 2, no. 1 (2021): None-None.

Harvard

Sifuna, K., Lwangale, D. W., Simotwo, P., Sifuna, K., Lwangale, D. W. and Simotwo, P. (2021) 'Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya' Himalayan Journal of Economics and Business Management 2(1), pp. None-None.

Vancouver

Sifuna K, Lwangale DW, Simotwo P, Sifuna K, Lwangale DW, Simotwo P. Influence of Leadership on Poverty Reduction in the Devolved Government in Trans-Nzoia County, Kenya. Himalayan Journal of Economics and Business Management. 2021 Jan;2(1):None-None.

Wibowo, J. G., Aldianto, L. & Hutajulu, S. (2024). Loyalty Program for Digital Banking to Increase Active Rate: A Case Study of Rosemary Digital Banking. Himalayan Journal of Economics and Business Management, 5(1), 1-11.

MLA

Wibowo, Joseph G., Leo Aldianto and Sahat Hutajulu. "Loyalty Program for Digital Banking to Increase Active Rate: A Case Study of Rosemary Digital Banking." Himalayan Journal of Economics and Business Management 5.1 (2024): 1-11.

Chicago

Wibowo, Joseph G., Leo Aldianto and Sahat Hutajulu. "Loyalty Program for Digital Banking to Increase Active Rate: A Case Study of Rosemary Digital Banking." Himalayan Journal of Economics and Business Management 5, no. 1 (2024): 1-11.

Harvard

Wibowo, J. G., Aldianto, L. and Hutajulu, S. (2024) 'Loyalty Program for Digital Banking to Increase Active Rate: A Case Study of Rosemary Digital Banking' Himalayan Journal of Economics and Business Management 5(1), pp. 1-11.

Vancouver

Wibowo JG, Aldianto L, Hutajulu S. Loyalty Program for Digital Banking to Increase Active Rate: A Case Study of Rosemary Digital Banking. Himalayan Journal of Economics and Business Management. 2024 Jan;5(1):1-11.