Sustainable Development Goals (SDGs) as a global development agreement were ratified by world leaders officially on September 25, 2015, at the United Nations (UN) Headquarters. Approximately 193 heads of state attended, including Indonesian Vice President Jusuf Kalla who also endorsed the SDGs Agenda. Carrying the theme "Changing Our World: 2030 Agenda for Sustainable Development", the SDGs which contain 17 Goals and 169 Targets are a global action plan for the next 15 years (valid from 2016 to 2030), to end poverty, reduce inequality and protect the environment. SDGs apply to all countries (universal) so that all countries without exception developed countries have a moral obligation to achieve the SDGs Goals and Targets. The SDGs are a refinement of the MDGs,

One way for companies to show their contribution to the SDGs is by producing a sustainability report. A sustainability report is a report that contains information on the company's performance on economic, environmental, and social aspects which is carried out over one year. According to the Financial Services Authority (OJK), the preparation of this sustainability report also aims to communicate the company's commitment to running a sustainable business. Sustainability reports can also provide a broader and more open picture to all stakeholders regarding the sustainable development activities that have been carried out by the company. The number of sustainability report disclosures in Indonesia is still relatively low. As evidenced by the OJK, until March 2017, the number of companies listed on the IDX that had issued new sustainability reports was around 9%. Setyawan et al. [1] in his research also showed a low level of sustainability report disclosure, which can be seen from the average of the research object, which is 37.31%. In addition, Kusuma and Priantinah's research [2] also found low disclosure of sustainability reports, namely 33.20%. Company awareness to disclose voluntary reports such as sustainability reports is still lacking. According to Tobing et al. [3]. Another reason is that regulations governing sustainability reports in Indonesia only appeared in 2017 through POJK 51/POJK.03/2017. Company awareness to disclose voluntary reports such as sustainability reports is still lacking. According to Tobing et al. [3].

Company goals are an achievement that will be produced by a company. The company's targets are quantitative and the achievement of these targets is a measure by the success of the company's performance. As time passed, slowly the concept of corporate objectives is not only to achieve target numbers but also to fulfill environmental responsibility as a result of the company's operational activities. Participating in sustainable development is a major issue around the world for now. Not only in developed countries but also in developing countries which are struggling to prosper the economy, while the existing resources and environment decrease or shrink [4].

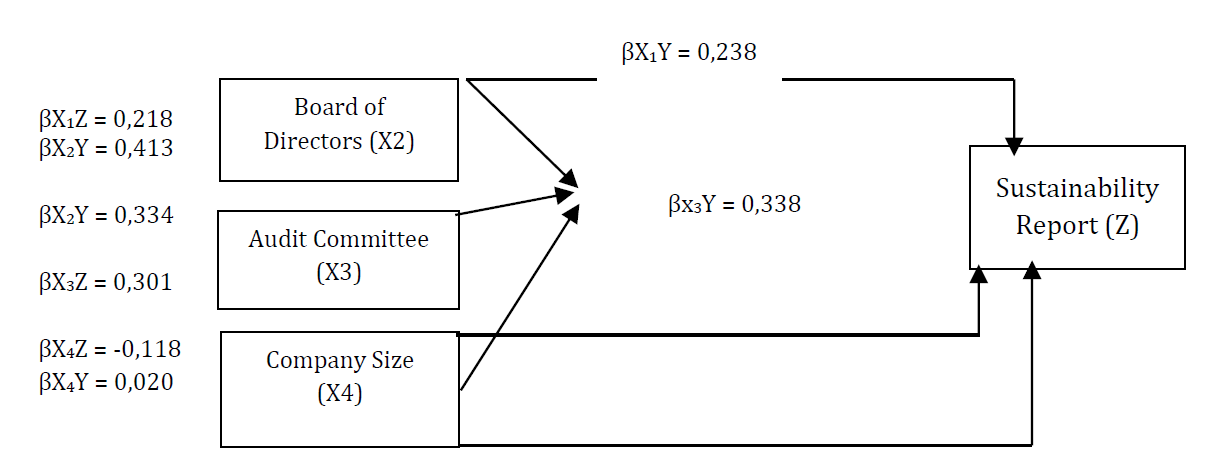

Discussing about the sustainability report, several things influence it. Research on disclosure of sustainability reports has been carried out by several researchers, research by Aliniar [5], Afsari et al. [6] and Nurleni et al. [7] stated that there is a positive relationship between institutional ownership variables and disclosure of sustainability reports. Meanwhile, Roviqoh and Khafid and Madani and Gayatri's research [8] reveal that institutional ownership does not affect sustainability reports. Justin and Suprajitno [9] show that the structure of the board of directors influences the disclosure of sustainability reports, while Hasanah et al. [10] state the opposite that the board of directors does not affect the disclosure of a sustainability report. Afsari et al. [6], Leksono, and Buallay and Aldhaen [11] that the audit committee influences the disclosure of sustainability reports. while the results of research conducted by Roviqoh and Khafid [12], Aliniar and Wahyuni [5], Hasanah et al. [10], and Tobing et al. [3] resulted in research that the size of a company's audit committee has no significant positive effect on the quality of sustainability report disclosure. Madani and Gayatri [8], Afsari et al. [6], Damayanti and Hadiningsih [13], Kelvin et al. and Tobing et al. [3] that company size influences the disclosure of Sustainability reports. Meanwhile, Roviqoh and Khafid [12], Aliniar and Wahyuni [5], and Leksono told that company size does not affect the disclosure of Sustainability reports. Institutional ownership is considered a factor that can affect profitability [14] as well as research produced by Fitria et al. and Nurkin et al. [15]. However, Rofiqoh and Khafid [12] and Situmorang and Simanjuntak [16] show conflicting results that institutional ownership does not affect profitability. The board of directors is one of the factors that can affect profitability according to research conducted by Rumapea, Fitriyani [17], and Fitria et al. While the conflicting results were concluded by Situmorang and Simanjuntak [16] who stated that the size of the board of directors did not affect profitability. Roviqoh Research and Khafid [12] and Fitriyani [17] and Rumapea conclude that audit committees affect profitability. However, Suryanto and Refianto [14] concluded in their research that the audit committee does not affect company profitability. Company size can affect a company's ability to generate profit or profit (profitability) [18] and Roviqoh and Khafid [12] say the same thing. While the opposite result that there is no effect between company size on profitability is stated in the research of Aghnitama et al. [19]. Roviqoh and Khafid [12], Madani and Gayatri [8], Leksono, and Tobing [3] in their conclusions explain that profitability affects the disclosure of sustainability reports.

This research is interesting to do because of the research gap described above. Previous research used financial reports and Sustainability reports for the year where the OJK had not issued rules regarding sustainability reports through POJK 51/POJK.03/2017, while this research used financial reports after these rules were published. The population in this study are companies listed on the LQ-45 Index because it is a composite index of 45 issuers with high liquidity, in selecting issuers to be included in the LQ 45 index, the selection is carried out with several selection criteria [20].

Literature Review and Hypothesis Development

Agency Theory: Agency theory is a theory that explains the relationship that occurs between the management of the company as an agent and the owner of the company as the principal. The principal is the party that gives orders to other parties, namely agents, to carry out all activities on behalf of the principal [21] this theory concerns the relationship or contract between the principal and the agent. The principal is the power of a large number of shareholders, whose interest conflict with those of managers, as a result, the company shows the separation of ownership and control, by modeling the company as two rational individuals with conflicting interests. This conflict causes agents to act inconsistently with the interests of the principal, thus triggering agency costs [14]. As an agent, the manager of a company, if you want to get compensation according to the contract, the manager must optimize the profits of the principals.

Agency theory includes disclosure of sustainability reports that can minimize information asymmetry between agents and owners. Institutional ownership is the number of external institutions that have shares in the company. The size of institutional ownership can influence investor control over management to disclose a sustainability report. This is important as a form of company transparency over information which contains actions that have been taken to maintain the company's condition from an economic, environmental, and social perspective.

Legitimacy Theory

Legitimacy is an acknowledgment of the legality of something. Organizational legitimacy can be said as a potential benefit or source for the company to survive [22]. According to this theory, a company operates with permission from the community, where this permit can be withdrawn if the community judges that the company has not done the things that are required of it.

Republic of Indonesia Law number 40 of 2007 concerning Limited Liability Companies states that social and environmental responsibility is the company's commitment to participate in sustainable economic development to improve the quality of life and a beneficial environment, both for the company itself, the local community, and society in general. Setiawan et al. the problem with the disclosure of sustainability is how much data related to environmental, social, and corporate governance practices and impacts must be disclosed. A company must carry out company activities by established rules to get support from the wider community.

Stakeholder Theory

Stakeholder theory has undergone a change in definition over the past few years. Friedman [23] said that the main goal of the company is to maximize the prosperity of the owner. This shows that the definition of stakeholder initially only refers to the owner of the company. However, Friedman [23] broadens the definition of stakeholders to include more constituencies, including groups that are not profitable for the company. Damayanti and Hardiningsih [13] define stakeholders as parties who have an interest in the company and can influence company activities. The parties referred to as stakeholders are the community, employees, government, suppliers, capital markets, and others.

Institutional Ownership

Institutional ownership is the percentage of share ownership by institutions or institutions such as insurance companies, banks, investment companies, and other institutional owners. Theoretically, the higher the institutional ownership, the stronger the control over the company, the company's performance/value will increase if the company owner can control management behavior so that it acts by company goals [25]. Institutional ownership will encourage more optimal monitoring of management performance, especially in decision making

Audit Committee

According to Rule Number IX.1.5 in the Decree of the Chairman of BAPEPAM Number: Kep-643/BL/2012, ―Audit Committee is a committee established by and responsible to the Board of Commissioners in assisting the carrying out of the duties and functions of the Board of Commissioners. It was concluded that the Audit Committee is a committee formed by the Board of Commissioners which has the duties and responsibilities of assisting the Board of Commissioners in carrying out internal oversight, ensuring the effectiveness of internal auditors and external auditors, and strengthening auditor independence. In Article 1 paragraph (1) of OJK Regulation 55/2015, an audit committee is a committee formed by and is responsible to the board of commissioners in assisting in carrying out the duties and functions of the board of commissioners.

Company Size

Company size has an influence on the company in terms of the ability to bear the consequences of various situations that the company will face [26]. Large companies generally have large resources, so the companies need and can finance information for internal purposes as a whole. On the other hand, small companies require greater additional costs if the company wants their information to be disclosed comprehensively. Theoretically, large companies will not be free from pressure, and larger companies with operating activities and greater influence on society will probably have shareholders who pay attention to social programs made by the company so that disclosure of the company's Sustainability report will be wider.

Profitability

Profitability is the ability of a company to earn a profit (profit) in a certain period [27]. The company is claimed to be good if the company can obtain large profits according to the expectations of owners and investors. Profitability is a company's ability to generate profits [28]. The ultimate goal to be achieved by a company is maximum profit. Companies that get maximum profits can prosper as owners, and employees, and can improve product quality and make new investments [29].

The profitability ratio is one of the important indicators to assess the performance of a company. According to Sartono [30], profitability is the company's ability to earn profits from sales, total assets, and own capital. Thus, long-term investors will be very interested in this profitability analysis, for example, shareholders will see the benefits that will be received in the form of dividends.

Based on the Financial Services Authority Regulation [31] the audit committee acts independently in carrying out its duties and responsibilities. Audit committee members are appointed and dismissed by the board of commissioners. The audit committee consists of at least 3 (three) members from independent commissioners and parties from outside the securities company. The audit committee must be chaired by an independent commissioner who is also a member of the audit committee.

Disclosure of Sustainability Report

Sustainability reports have various definitions, according to Susanto and Tarigan [32], SR means reports that contain not only financial performance information but also non-financial information consisting of information on social and environmental activities that enable companies to grow sustainably (sustainable performance). Sustainability reports are also used by government institutions, for example from the Ministry of Environment to assess the company's performance towards the environment in every organizational disclosure. As is the case in Indonesia, regulations on CSR disclosure can be found in regulations issued by Bapepam and Law number 40/2007 concerning Limited Liability Companies.

Companies that are listed on the stock exchange should make disclosures that are open to the public (investors or potential investors). The problem with sustainability disclosure is how much data related to environmental, social, and corporate governance practices and impacts should be disclosed. According to data from OJK [33], sustainable disclosure in Indonesia is voluntary disclosure. In contrast to disclosures such as annual reports and financial reports which are mandatory for companies, especially companies with public status (listing on the stock exchange). Where the number of issuers is still smaller than non-public companies, only a few issuers on the IDX publish sustainability reporting [34].

The obligation to disclose sustainability reports is regulated more strictly in POJK No.51/POJK.03/2017 concerning the Implementation of Sustainable Finance for Financial Services Institutions, Issuers, and Public Companies. This POJK mentions the meaning of a sustainability report and sustainable finance. A sustainability report is a report announced to the public that contains the economic, financial, social, and environmental performance of an FSI, Issuer, and Public Company in running a sustainable business. Meanwhile, sustainable finance is comprehensive support for financial services to create sustainable economic growth by aligning economic, social, and environmental interests.

This POJK is one of the mechanisms to ensure that Sustainability Report reporting has a deterrent effect if it is not carried out by the company. Article 2 still in POJK No.51/POJK.03/2017 states that "LJK, issuers and public companies are required to implement sustainable finance in the business activities of LJK, issuers and public companies" meaning that sustainability reports can be implemented by companies and are something mandatory. Article 2 becomes one of the articles strengthening not only managing companies such as mining but banks also responsibility in disclosing sustainability reports.

Hypothesis

Institutional ownership is share ownership by the government, financial institutions, legal entity institutions, foreign institutions, transfer funds, and other institutions at the end of the year [14]. The institution is one of the shareholders in a company, where the composition of share ownership is determined by the percentage of share ownership [8]. Theoretically, the stronger the control within a company, which is influenced by the high institutional ownership [25]. According to agency theory [21], one way to reduce agency costs is to increase institutional ownership in the framework of monitoring managers. Corporate transparency from an environmental and social perspective must be maintained not only from an economic perspective, where the company's operational activities do not harm the environment [12]. Aliniar [5], Afsari et al. [6], and Nurleni et al. [7] concluded that there is an effect of institutional ownership on the disclosure of sustainability reports.

Institutional Ownership Affects the Disclosure of Sustainability Reports

Situmorang and Simanjuntak [16] argue that institutional ownership acts as a party that acts as a party that professionally monitors the development of investments invested by shareholders. Company owners can control or control the behavior of management in carrying out their duties so that the performance or value of the company will increase [25]. The greater the institutional investment, the investor will play a significant role in monitoring management performance. In Agency Theory, the ownership structure is considered capable of influencing company profitability [12], as a result, institutional ownership can affect profitability (Suryanto and Refianto, 2019) as well as research produced by Fitria et al. and Nurkin et al. [15].

Institutional Ownership Affects Profitability

The size of a larger board of directors has a wider range of resources and opportunities compared to a smaller board this is because the decisions of the board of directors will be better because there are many experienced board directors, so there are more board directors then the decision will be increasingly unaffected. The results of research by Justin and Suprajitno [9] show that the structure of the board of directors influences the disclosure of sustainability reports. Of the three variables studied (size of the board of directors, representation of female directors, and ownership of the board of directors), it is evident that the size of the board of directors has a positive effect on the disclosure of the Sustainability report [14]. shows that the board of directors influences the disclosure of the Sustainability report. Fitria et al. and Nurkin et al. [15] show that the board of directors affects the disclosure of the Sustainability report. Based on the description above, the hypothesis is formed as follows:

The Board of Directors Influences the Disclosure of the Sustainability Report

The board of directors can affect the effectiveness of monitoring activities [16]. Based on Agency Theory where more and more boards of directors in the company will provide a form of oversight that can minimize information asymmetry (Information Asymmetry). Information that allows fraud or errors in accounting procedures to occur will be minimized by having a board of directors. The company's performance will increase which is marked by increased company profitability. The board of directors is one of the factors that can affect profitability according to research conducted by Rumapea, Fitriyani [17], and Fitria et al. Based on the description above, the hypothesis is formed as follows:

The Board of Directors Affects Profitability

The audit committee is a committee appointed by the company as a liaison between the Board of directors and external audit, internal auditors, and independent members [5]. Roviqoh and Khafid [12] in taking on their responsibilities, the audit committee must coordinate. This communication is the duty of the audit committee in charge its duties to supervise management in reporting company performance results. Based on the Stakeholder Theory, information transparency made by company management can be maximized due to encouragement from the audit committee so that the information is following the needs of stakeholders. Sustainability reports are a form of the company's commitment to social issues and environmental issues to stakeholders [6]. This results in the establishment of good relations between the company and outsiders and the company's image will be good. In line with the conclusions of Afsari et al. [6], Leksono, and Buallay and Aldhaen [11] that the audit committee influences the disclosure of sustainability reports. Based on the description above, the following hypothesis is formed

The Audit Committee Influences the Disclosure of the Sustainability Report

Regular meetings are held by the audit committee to discuss problems that occur within the company [12]. Based on agency theory, this meeting is expected to reduce information asymmetry, which can become a problem. Problems that occur can be in the form of the possibility of inappropriate accounting procedures or even data manipulation. The more the number of the board of directors is in line with the increase in profitability. Research by Roviqoh and Khafid [12], Rumapea, and Fitriyani [17] show that the audit committee affects profitability. Based on the description above, the following hypothesis is formed

The Audit Committee Affects Profitability

Firm size has an influence on the company in terms of the ability to bear the consequences of various situations that will face by the company [26]. On the other hand, small companies require greater additional costs if the company wants their information to be disclosed comprehensively. So, it can be assumed that small companies face less political pressure compared to large companies. One of the levels of investor confidence is determined by the size of the company. Large companies have the consequence of getting more attention from the public as the company's influence on society and the environment [12]. Based on legitimacy theory, as the owner of resources that will later be used by a company, the company must obtain permission from the community in carrying out its operations. The size of the company will require it to carry out social and environmental activities. Madani and Gayatri [8], Afsari et al. [6], Damayanti and Hadiningsih [13], Kelvin et al. and Tobing et al. [3] state that company size influences the disclosure of sustainability reports. Based on the description above, the following hypothesis is formed: Kelvin et al. and Tobing et al. [3] state that company size affects Sustainability report disclosure. Based on the description above, the following hypothesis is formed: Kelvin et al. and Tobing et al. [3] state that company size affects Sustainability report disclosure. Based on the description above, the following hypothesis is formed:

Company Size Affects Sustainability Report Disclosure

The size of operational activities within the company can be reflected in the size of the company, large companies can produce on an economic scale, as a result, the products produced have low unit prices, this low unit price makes the company have high competitiveness in the market [12]. As a result, there is an increase in the company's sales, which in turn increases the company's profits. Thus, large-scale companies have more opportunities to increase their profitability. Based on stakeholder theory, increasing profitability is the responsibility of the company to meet the expectations of all stakeholders. So, company size can affect a company's ability to generate profit or profit (profitability) [18] and Roviqoh and Khafid [12] and say the same thing. Based on the description above, the following hypothesis is formed:

Firm Size Affects Profitability

The profitability ratio is an important indicator for assessing a company's performance, this ratio is used to assess a company's ability to make a profit. as well as provide a measure of the effectiveness of the management of a company [3]. Thus, long-term investors will be very interested in this profitability analysis, for example, shareholders will see the benefits that will be received in the form of dividends. Revealing the sustainability report and the size of a company's profitability is important. The ability of a company to earn more profit is a reference that the company can be said to be financially healthy [12]. Based on the theory of legitimacy stated that to create conditions that are acceptable to society and the environment, the company will try to meet the needs of stakeholders, including information needs that are manifested through the disclosure of sustainability reports. Roviqoh and Khafid [12], Madani and Gayatri [8], Leksono, and Tobing [3] in their conclusions explain that profitability affects the disclosure of sustainability reports. Based on the description above, the hypothesis is formed as follows: Leksono and Tobing [3] in their conclusions explain that profitability affects the disclosure of sustainability reports. Based on the description above, the hypothesis is formed as follows: Leksono and Tobing [3] in their conclusions explain that profitability affects the disclosure of sustainability reports. Based on the description above, the hypothesis is formed as follows: